The Impossible Triangle at the Heart of Big Law

Legalweek 2026 closed with a final-day keynote that didn't sugarcoat anything. Titled The Reckoning: Why Yesterday's Playbook Won't Guarantee Tomorrow's Success, the session delivered by Patrick Fuller, Law.com's Chief Legal Industry Strategist, and Heather Nevitt, Editor-in-Chief of Corporate Coverage, was equal parts forensic data analysis and strategic wake-up call. It was the kind of presentation that makes you quietly reconsider your entire firm's five-year plan before you've finished your morning coffee.

The visual anchor for the entire keynote? A Penrose triangle—the famous "impossible object" created by Lionel Penrose and his son Roger in 1958. Each corner appears structurally sound. The geometry looks correct. But the whole shape cannot actually exist in three-dimensional space. Fuller and Nevitt used this as the throughline for their argument: the legal industry's key metrics—rate increases, rising profits per equity partner, growing headcount—each look solid in isolation. But follow the geometry all the way around, and the structure is an illusion.

Two Companies, One Lesson: The Power of Self-Disruption

Before a single data slide appeared, Fuller and Nevitt took the audience back to the late 1990s and early 2000s with two stories that framed the entire discussion: Apple and Netflix.

Apple: Killing the iPod on Purpose

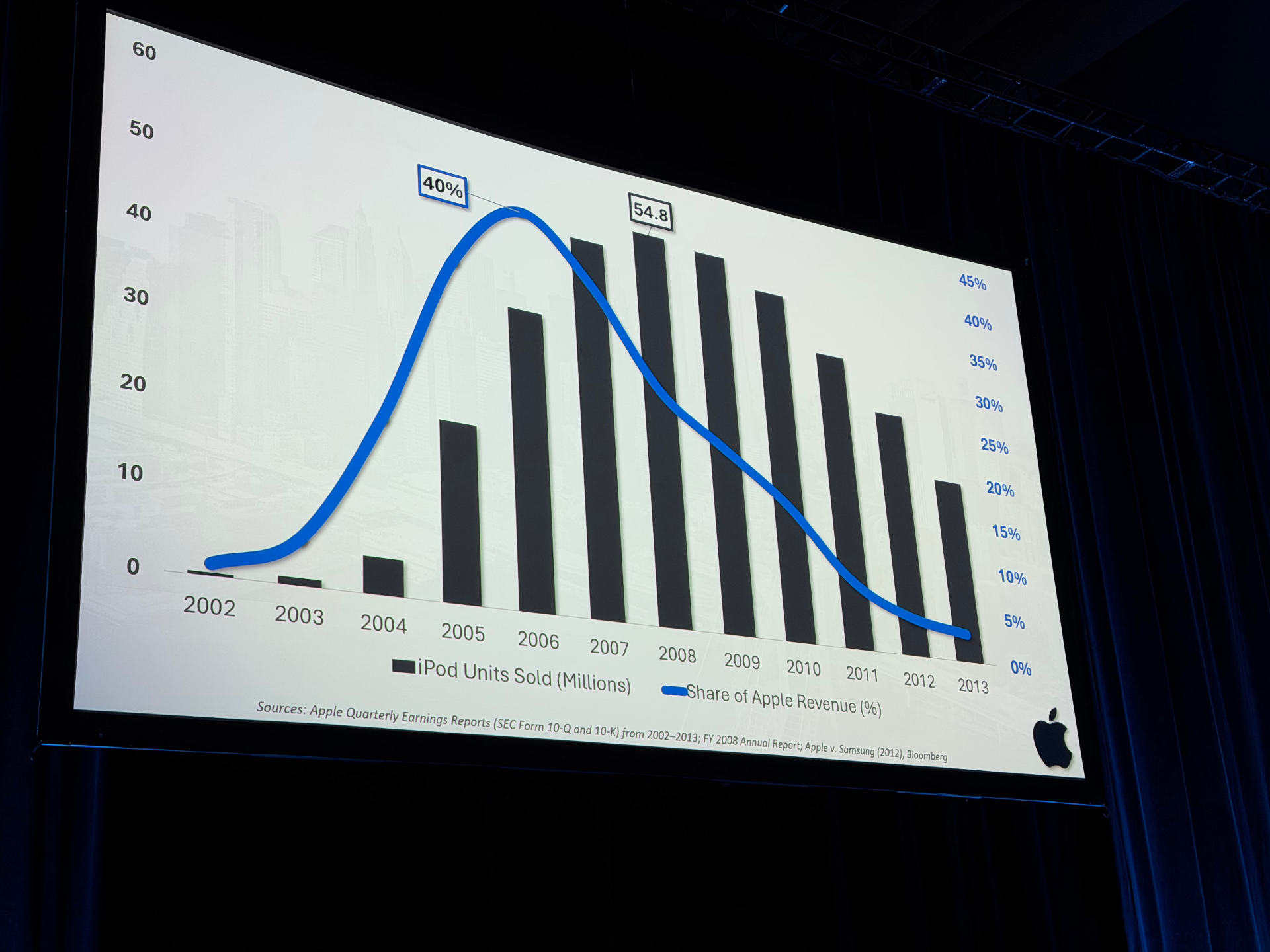

Apple came into the 2000s bruised. Microsoft had dominated the prior decade, and Apple faced the genuine prospect of becoming, as Fuller put it, "the Kodak of home computers." The iPod changed everything. By 2006, it represented a staggering 40% of Apple's total revenue, peaking at 54.8 million units sold in a single year.

But in 2004, while iPod sales were still surging, Steve Jobs quietly launched Project Purple—a secret internal initiative to build a touchscreen device that could make calls, store music, play movies, and completely upend the software delivery model. If it worked, it would make the iPod—Apple's lifeline—obsolete.

It worked. The iPhone launched in 2007. iPod's share of Apple revenue began a terminal decline and by 2013 was essentially a rounding error. Apple didn't mourn the iPod. They had already moved on—because they were the ones who decided to move on.

Netflix: Cannibalizing the Red Envelope

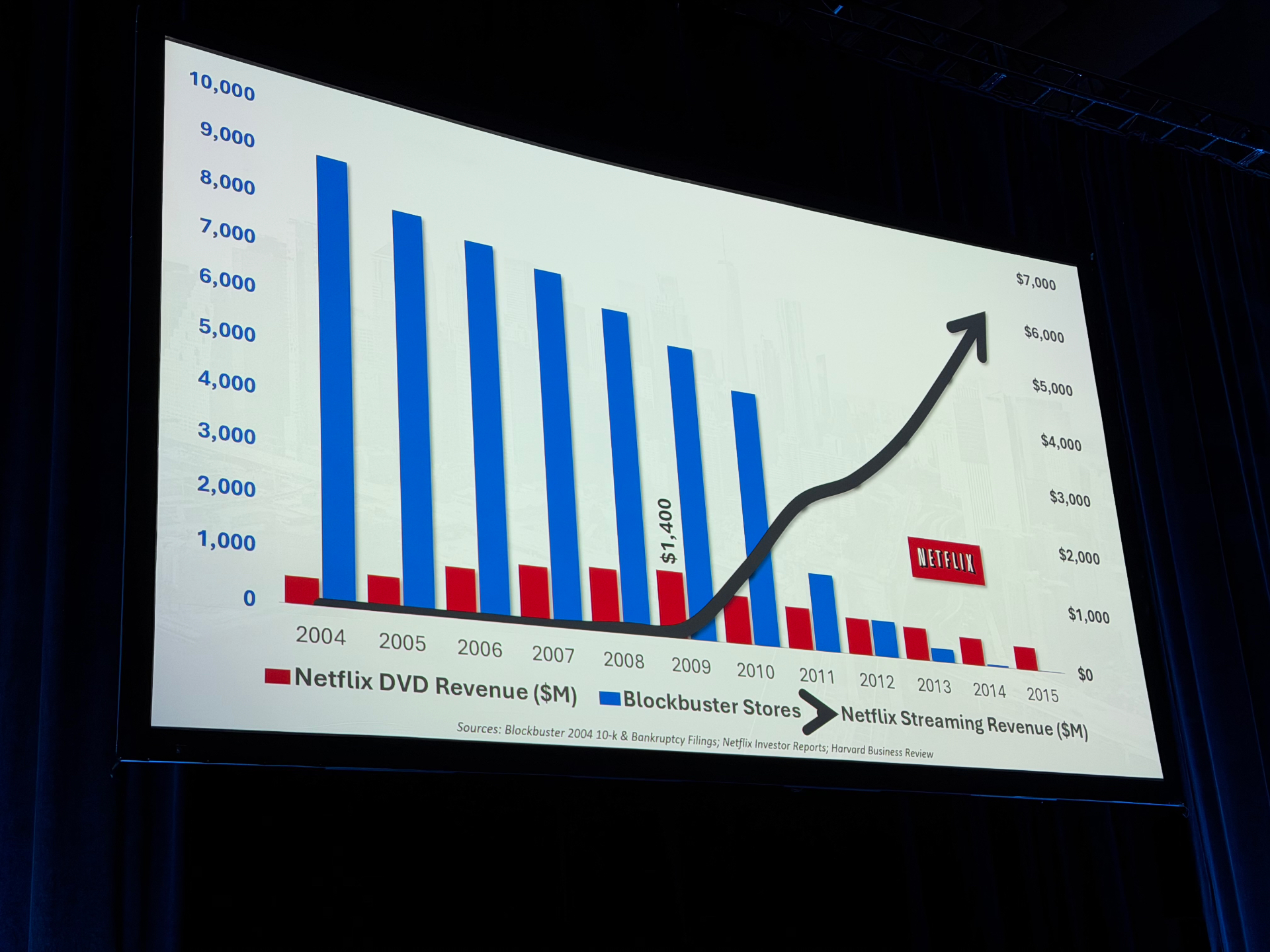

Netflix was the mirror image. While Blockbuster commanded 9,000 physical stores, Netflix had a website and a warehouse. But in 2004, with DVD-by-mail revenue still growing, Reed Hastings began building streaming infrastructure for a market that barely existed—broadband penetration was limited and data caps were common.

In 2007, Netflix launched "Watch Instantly" as a streaming add-on. By 2010, it was a standalone service. Blockbuster's store count, which had been quietly eroding, collapsed. Nine thousand stores became essentially zero within a few years, while Netflix streaming revenue went nearly vertical.

The keynote's critical insight: neither Apple nor Netflix waited for their existing businesses to show signs of failure before building the replacement. They cannibalized themselves while the business was still working. They made the uncomfortable bet before they had to. That is the challenge now sitting on every managing partner's desk.

The Am Law 200: A Cautionary Census

Fuller brought the disruption story directly to the legal industry with a striking piece of data: of the 200 firms on the inaugural Am Law 200 ranking published in 1999, 74 firms—37% of the original list—no longer exist as ranked entities. They have merged, dissolved, or collapsed.

These weren't just lower-tier firms. The casualties included one firm from the top five, four from the top 25, and 30 from the Am Law 100. Collectively, those 74 departed firms represented 27% of the total revenue from the original 1999 ranking.

Am Law 200 Attrition — 1999 to 2026

"Status is not a strategy, and presence is not protection." — Patrick Fuller

From Binary Choices to Ternary Strategy

One of the keynote's most compelling frameworks was the concept of ternary strategy—a rejection of the binary "build vs. buy" thinking that has dominated legal industry conversations for years. The real strategic question, Fuller argued, isn't how you respond to disruption. It's which disruption you choose to lead. Firms face three paths: disrupt the market, self-disrupt, or be disrupted.

The In-House Perspective: Composure Under Fire

Nevitt's portion of the keynote shifted focus to what's happening inside legal departments. Her central observation: after half a decade of rolling crises—pandemic, regulatory whiplash, geopolitical instability, tariff uncertainty—general counsel are no longer in reactive mode. They have structurally absorbed the chaos.

The surprise, she noted, isn't the strain. It's the composure. Legal leaders have accepted that volatility is not episodic—it is structural. One global GC she quoted put it this way: the constant pace has become the norm.

A Redefinition of Purpose

Nevitt framed the in-house transformation around three pivots: from reactive to proactive, from bespoke to scalable, and from siloed to integrated. Legal departments are no longer artisanal shops custom-crafting every response. They're building playbooks, templates, and automated workflows so human judgment can be reserved for the highest-value decisions.

She was emphatic that the differentiator isn't the smartest AI model or the fastest deployment. It's two irreplaceable human capacities: leadership through change and ethical judgment—the ability to ask who benefits, what risk is created, and what trade-offs are acceptable. A Lexology Pro survey she cited found that two-thirds of in-house counsel don't feel fully equipped in either area—a gap that is simultaneously a massive opportunity.

AI in the Department: Momentum with the Brake Hovering

On AI adoption, the data paints a picture of enthusiastic but cautious deployment. Ninety percent of in-house counsel report increased efficiency when using AI tools. But the number one barrier to deeper adoption remains unclear ROI—teams can feel the speed gains but struggle to quantify them in the language of finance.

The Rate Illusion: Growth That Isn't

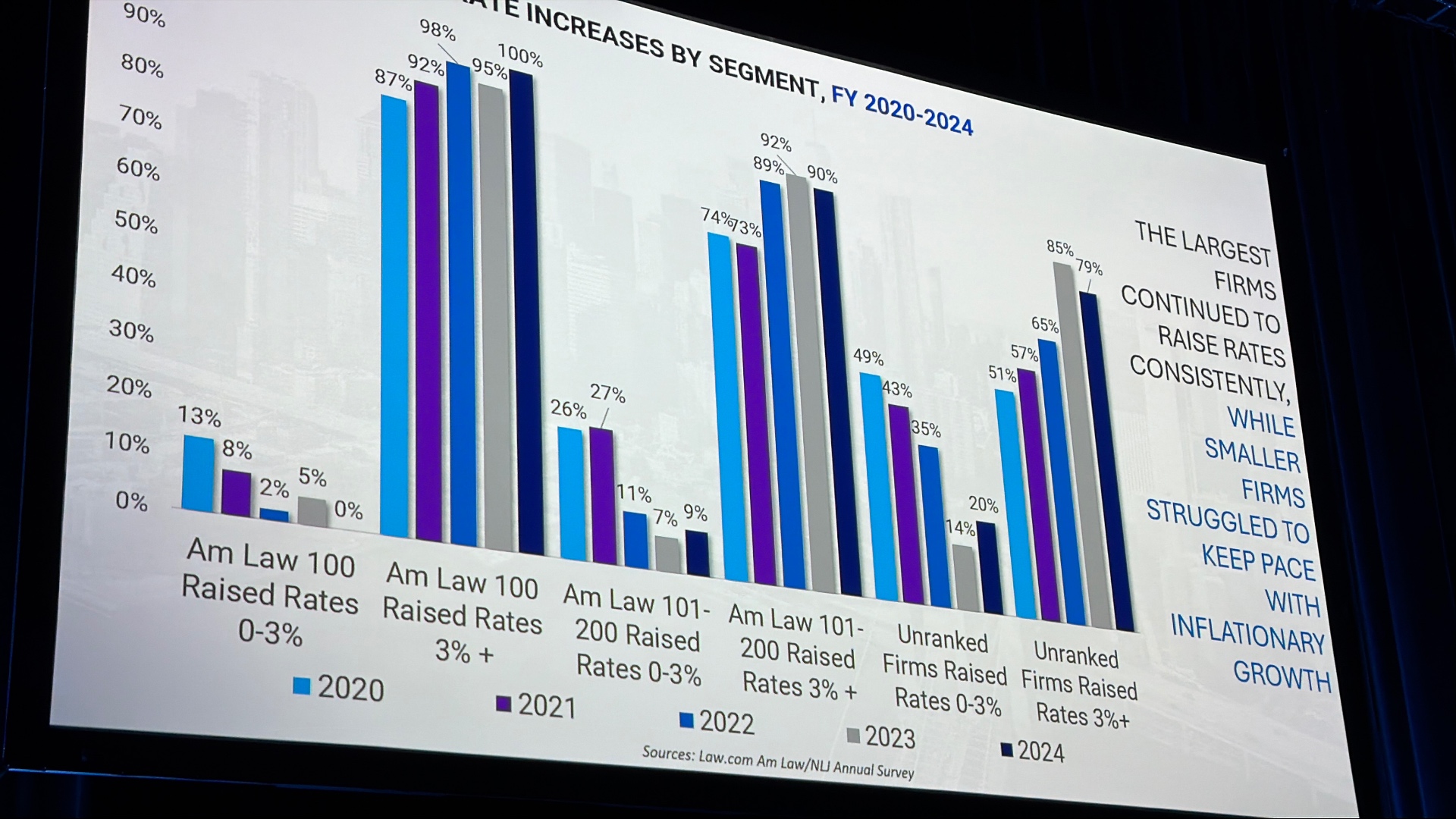

Fuller returned with a deep dive into billing rate data from FY 2020–2024 across the Am Law segments, and this is where the keynote's Penrose triangle metaphor really crystallized.

The headline looks triumphant: by 2024, 100% of Am Law 100 firms reported raising rates by 3% or more. But the further down-market you look, the more inconsistent the picture becomes. Am Law 101–200 firms raised rates unevenly. Unranked firms struggled to clear basic inflationary thresholds even in a year when costs were rising across the board.

Fuller called this a "behavioral problem masquerading as a pricing problem." Mid-market and unranked firms aren't under-pricing because their value isn't there. They're under-pricing because loss aversion—the fear of losing a client—feels more immediate than the slow bleed of profit erosion.

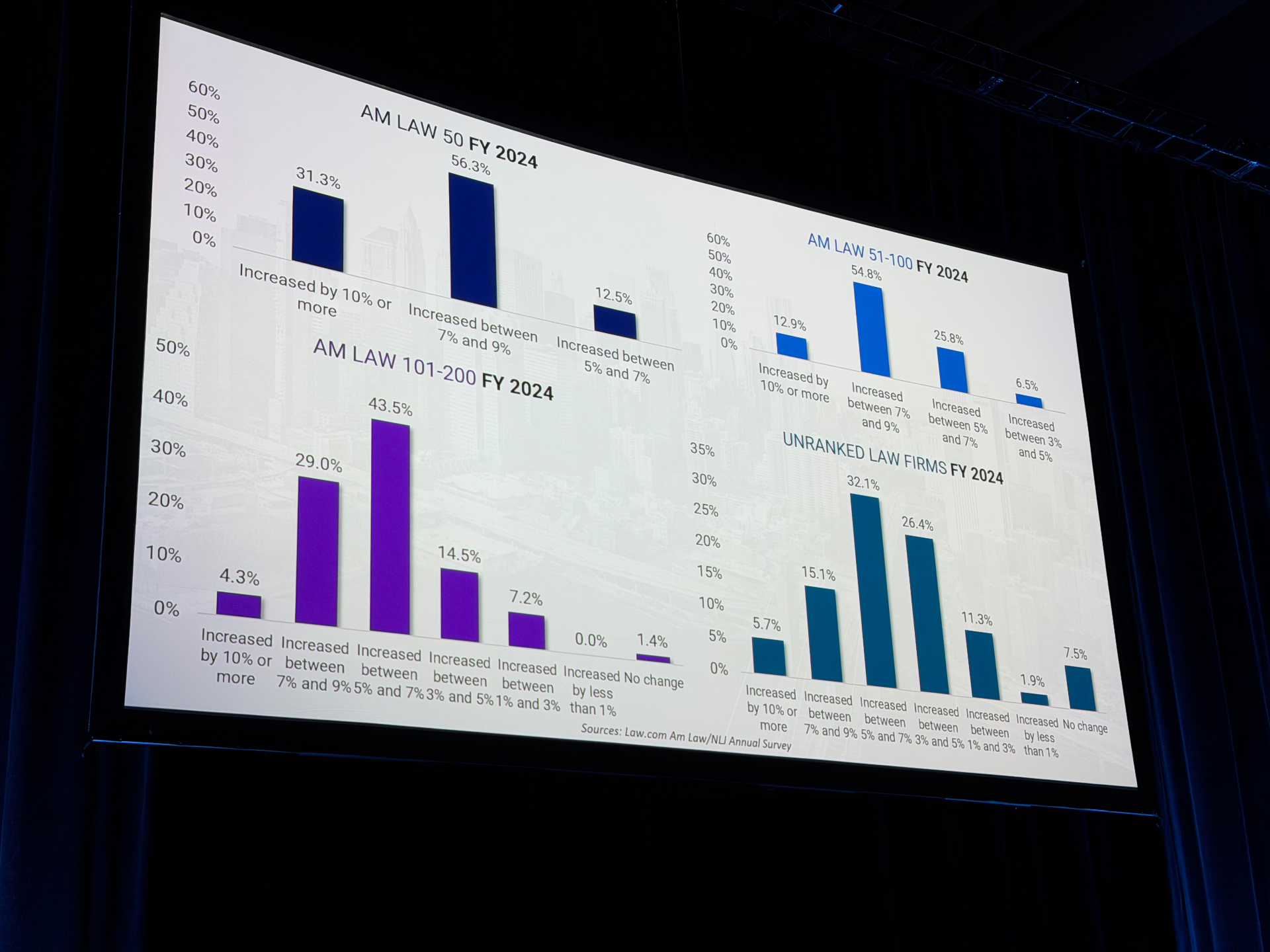

Am Law 50: A Different Planet

The Am Law 50 FY 2024 breakdowns told a dramatic story. Over 31% of Am Law 50 firms raised rates by 10% or more, and another 56% raised them between 7–9%. These firms didn't ask for permission. They operated on a simple premise: clients expect excellence and will pay for it.

Adjust for Inflation, and the Geometry Breaks

The most sobering slide of the keynote came when Fuller applied the GDP implicit price deflator to five-year compound annual growth rates. This is the microscope that reveals whether nominal growth is real growth or just a hamster wheel.

| Metric | Reality Check |

|---|---|

| Revenue per Lawyer | Am Law 50 barely positive at 0.7% in real terms. Everyone else is flat or negative. More lawyers plus flat demand = math doesn't work. |

| Profits per Equity Partner | Am Law 50 growing at 4.4% inflation-adjusted — but engineered through equity tier compression. FY 2024: first year non-equity partners outnumbered equity partners in Am Law 100. |

| Profits per Lawyer | Only the Am Law 50 is positive after inflation. Everyone else is losing ground in real dollars. |

"Several firms are financing the appearance of prosperity while profitability, measured in real inflation-adjusted dollars per lawyer, is quietly eroding. That's not a headline from our editorial team. That's a warning from our consulting arm." — Patrick Fuller

Talent Wars and the Consolidation Tsunami

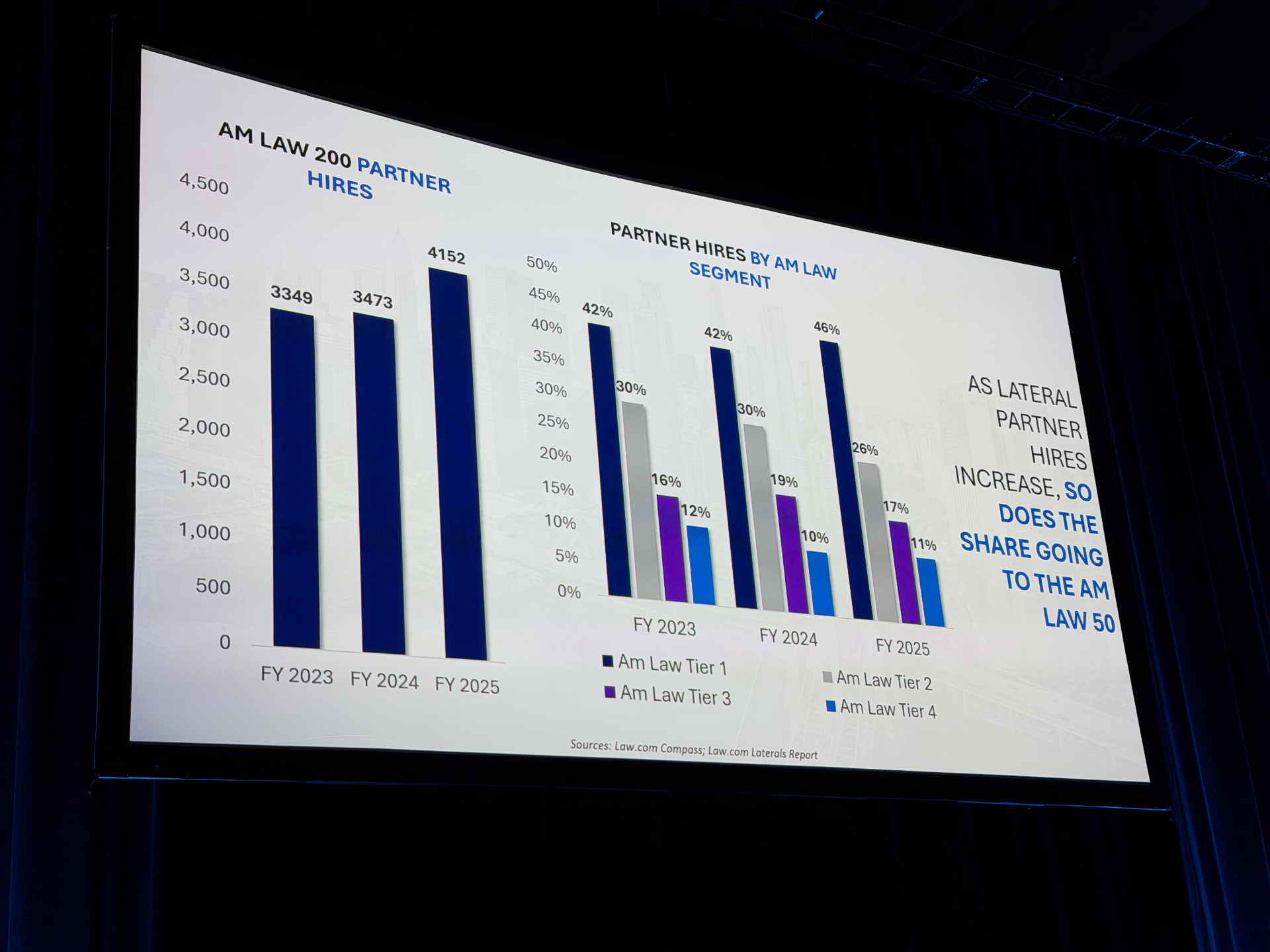

Nevitt presented data on lateral partner hiring that underscored the consolidation theme. Am Law 200 lateral partner hires rose from 3,349 in FY 2023 to 4,152 in FY 2025—a 20% increase in two years, which, in a profession that moves slowly, qualifies as seismic.

But where are those laterals going? The Am Law 50 captured 42% of lateral hires in FY 2023. By FY 2025, that share had climbed to 46%. The largest firms aren't just raising rates more aggressively—they're winning the talent market more aggressively too.

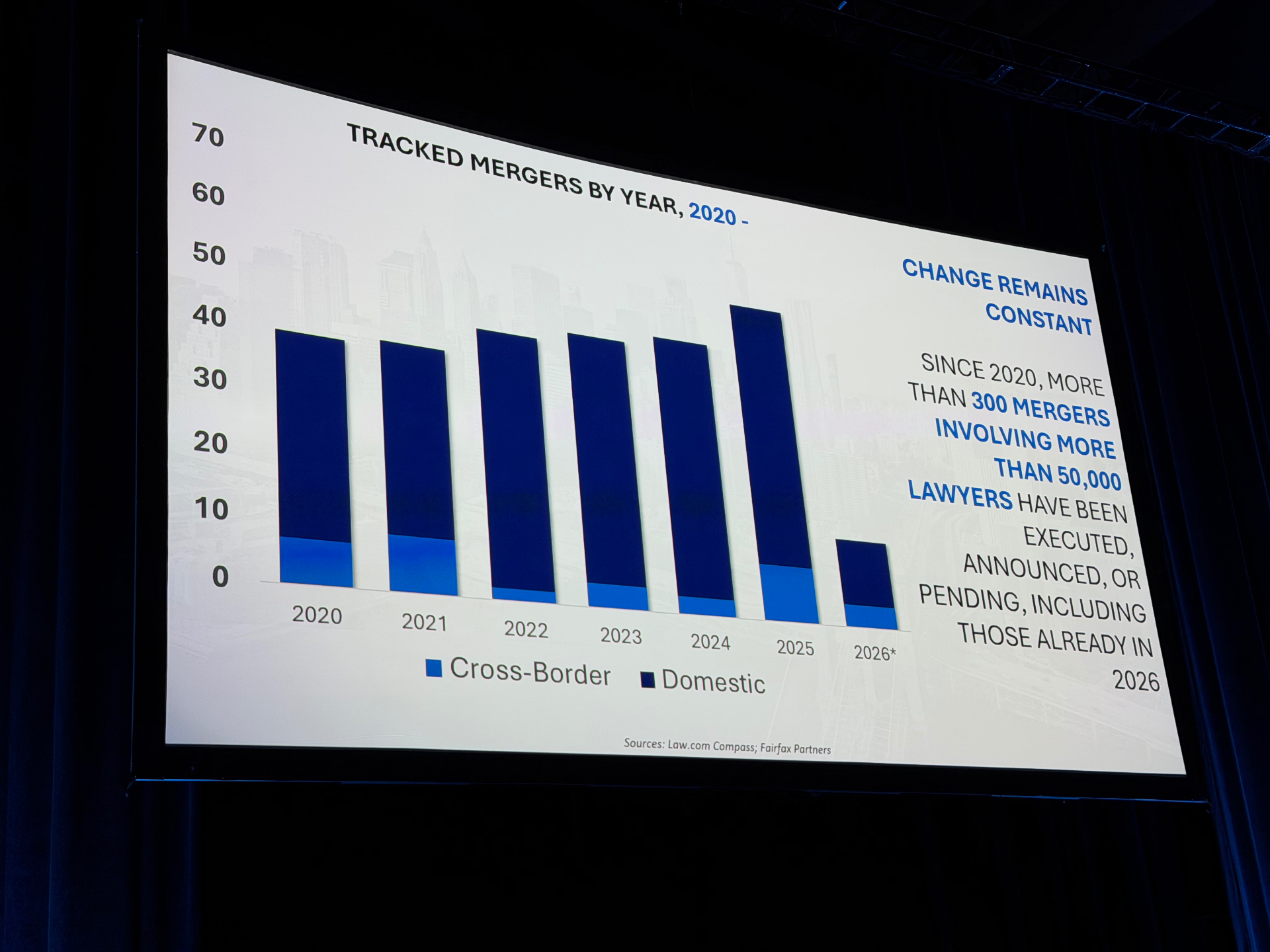

Since 2020, more than 300 mergers involving over 50,000 lawyers have been executed, announced, or are pending. 2025 was the most active year in the range, and 2026 was already tracking significant activity only three months in.

The AI Conviction–Action Gap

Fuller introduced findings from a joint survey with Wicker Park, the leading client feedback consultancy, covering over 170 law firms. The results revealed a striking gap between belief and behavior.

On a 1–7 scale, firms rated AI's significance for competitive advantage over the next five years at a median of 6. Near consensus that AI will be a primary differentiator. And yet: only 46% of firms expect AI to produce net revenue growth. Twenty-four percent expect net revenue losses. Twenty-nine percent expect no change at all.

What Clients Actually Want

Seventy-five percent of law firms believe their clients are demanding faster, cheaper, and smarter—not one or the other, but all three simultaneously. Yet only 49% believe clients want proactive AI-driven insights and horizon scanning. Half of the profession is still primarily selling reactive legal services—exactly the zone where firms self-inflict wounds through excessive discounts and commoditization.

Nevitt distilled what corporate counsel want from outside partners into five priorities: efficiency through technology, transparency on AI use, outcome-oriented pricing, domain fluency and integration, and risk-aware innovation with guardrails. She cited Salesforce CLO Sebastian Niles' statement from earlier in the week that the era of AI pilots is over and that efficiency gains shared with clients are no longer optional.

"AI is not going to replace lawyers. But lawyers who build relationships and incorporate AI will absolutely replace lawyers who don't." — Heather Nevitt

Illusory Superiority and the GPS Without Roads

Perhaps the most uncomfortable data from the Wicker Park survey involved firm self-assessment. Firms rated their overall AI adoption progress at 4 out of 7—encouraging on its face. But when asked specifically about their lawyers' actual preparedness to use AI tools, that number dropped to 3.9. Same firms. Same survey. Different questions. A gap that reveals exactly where belief ends and reality begins.

Seventy-five percent of firms are offering AI training and upskilling. Sounds like progress—until you learn that 66% said they are not hiring the professional specialists needed to actually sustain that adoption.

"You can train people to peel an orange, but if you painted it blue and told everyone it's something else entirely, training alone isn't going to solve the problem." — Patrick Fuller

Firms are handing people a GPS and a map without building the roads. That's not an AI strategy. That's an AI announcement.

The Fee–Compensation–Technology Triangle: Still Impossible

Only 19% of firms have modified their fee engagements in any way to align with increased AI adoption. Seventy-two percent have no plans—or simply don't know whether they'll change attorney compensation structures to account for AI use.

Fuller mapped this back to the Penrose triangle: for technology-driven change to be sustainable, three things must align—fee engagements, behavioral incentives, and the technology itself. Advance any one without the others, and you've built the illusion of a triangle, not a real one.

"If your compensation plan is in conflict with your strategic plan, then your compensation plan is your strategic plan." — Tim Parker, via Patrick Fuller

The Productivity Paradox: Have the Patience to Let It Grow

The keynote's closing arc invoked economist Erik Brynjolfsson's "productivity paradox"—the well-documented lag between the arrival of transformative technology and its measurable impact on output. You invest. You wait. You question the investment. Your partners question it. And then, if you've built the right infrastructure, the gains arrive.

Apple and Netflix understood their own productivity paradoxes were coming. They planned for them. They didn't let short-term performance anxiety drive them back to the old model, even when shareholders and analysts were skeptical.

The legal industry is in the midst of its own productivity paradox right now. The seeds are in the ground. The question, as Nevitt put it, is whether firms have the patience and the strategic conviction to wait for them to grow.

Key Takeaways

Status Is Not a Strategy

37% of the original Am Law 200 are gone. They had status, history, and brand equity. None of it was a substitute for strategic adaptation.

Self-Disruption Is the Only Sustainable Advantage

Apple killed the iPod. Netflix killed the red envelope. Both did it while the business was still working.

The Penrose Triangle Is the Perfect Metaphor

Rate increases are up. PEP is up. Headcount is growing. But inflation-adjusted profits per lawyer tell a different story.

The Middle Market Is Under-Pricing Out of Fear

Loss aversion is contagious. Clients are more accepting of rate increases than lawyers assume.

In-House Has Fundamentally Changed

General counsel are no longer in crisis mode — they've absorbed the chaos structurally. They want proactive partners.

AI Conviction Without Structural Realignment Is Theater

Only 19% have adjusted fees and 72% haven't touched compensation. Without aligning pricing, incentives, and technology, it's an illusion.

The Question Isn't What You're Changing — It's What You're Willing to Redesign

Not adopted. Redesigned. That's the difference between bolting a new tool onto old workflows and building a genuinely new blueprint.

The closing question Fuller and Nevitt left with the room: What are you willing to redesign?

Save the Date: Legalweek 2027 — March 1–3, 2027 — North Javits Convention Center, New York City

Matthew A. Mishak, J.D.

Attorney • Founder, LegalTek.ai & SilverTung AI • MIT Sloan